Using customer segmentation to boost financial inclusion

How organisations can use the Fair4All Finance segmentation model to drive change and better serve more people in financially vulnerable circumstances

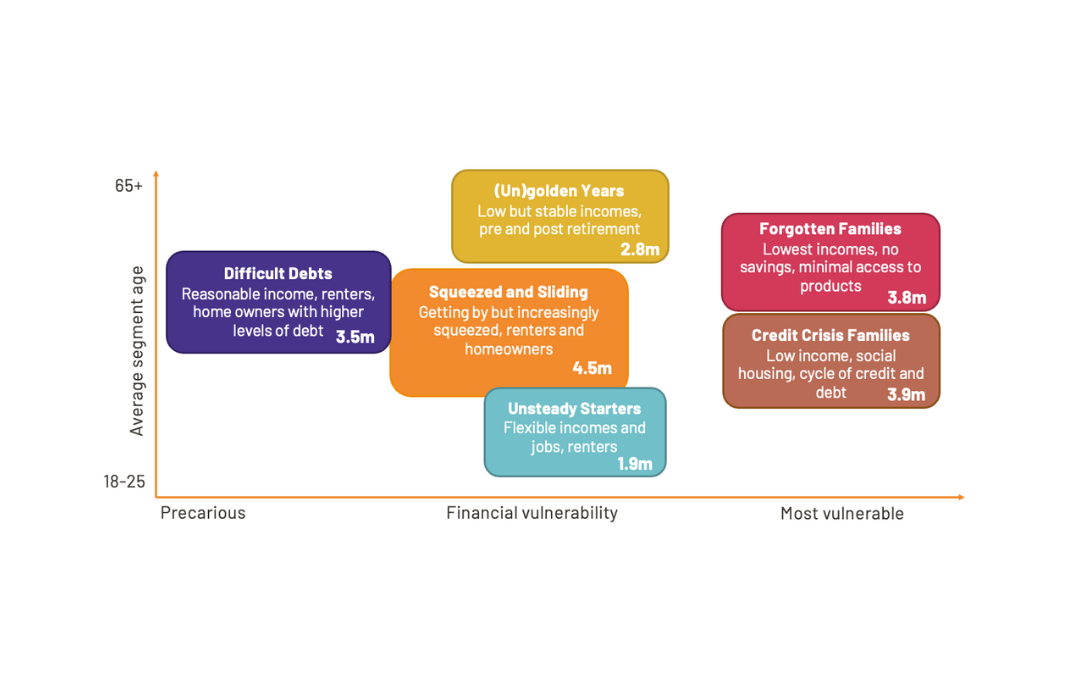

Our customer segmentation model was first released in 2022 and updated in 2024. It identifies over 20m people in financially vulnerable circumstances across six distinct segments, many of whom are currently under-served or excluded from the market.

In this blog we cover what segmentation is, how organisations can use it to boost inclusion and how our segmentation model differs from others.

You can also watch a recording of the session and Q&A we had on segmentation at our recent Building Financial Inclusion Together conference.

What is segmentation?

A customer, or user, segmentation is a common method for organisations to understand different groups of people with similar needs. They can then use this to design and deliver better propositions and services for each of those groups, rather than one homogenous audience. This can help with getting really focused on what a certain group of people needs.

Many organisations (especially large ones) will have their own segmentation model, either made up of their existing customers or the audiences that they want to serve.

At Fair4All Finance, we wanted to apply this methodology to understand the groups, and needs, of people in financially vulnerable circumstances. So that this can help all organisations design and deliver propositions and services that lead to better outcomes.

Who can use Fair4All Finance’s segmentation and how

Our segmentation shows 20.3m people in financially vulnerable circumstances. This is split across six segments, which range from 1.9m people to 4.4m people in size. For each segment we have a broad range of insights on their lives, financial lives and hopes and worries.

While the segmentation has given us a number of people in financially vulnerable circumstances, it’s not the primary reason we’ve built it. The segmentation is to help organisations understand who is experiencing financial vulnerable circumstances and what their needs are.

- This means the segmentation is most likely to be useful for:

- People who are responsible for designing and delivering propositions, products and services. This might include product and propositions teams as well as financial inclusion or customer vulnerability specialists

- Marketing teams who want to understand the priorities for each segment to inform their messaging, especially for community finance and other organisations who are already great at serving people in financially vulnerable circumstances

- Customer experience leads looking to design and deliver better journeys with regard to financial vulnerability

- Organisations, including researchers, who want information on specific areas to inform deeper or broader research design

Using the Fair4All Finance segmentation to drive change

Here are some examples of how organisations have used our segmentation model so far:

Understanding the needs of people impacted by rising costs

We have spoken with several organisations in the insurance sector who are interested to learn more about the rising costs of motor insurance, and who this might impact most.

There are several ways to do this. If an organisation wanted to look at households below a certain income threshold, for example £30,000, they could get the total size of this audience from ONS or other data. We know that this data set would include most of the people in Credit Crisis Families and Forgotten Families, as well as some across Unsteady Starters and (Un)golden years.

Our segments include information about employment, whether people use their car to get to work, and on the broader financial resilience of each segment. We can use it to look at existing levels of debt, savings and credit commitments, and hypothesise what this might mean for their ability to afford insurance in future.

This means organisations can understand how many people overall from nationally representative data, and the needs of the people impacted from the Fair4All Finance segmentation.

Better understanding current customer base to inform future strategy

A large financial services provider wanted to understand how the segments show up in their current customer base, and where they are more or less likely to serve groups of customers, to inform their financial inclusion strategy.

Working with us and CACI, they were able to understand where they were over or under represented with certain groups. This means that they can focus their strategy on segments that they already have access to, and design and deliver propositions to improve their financial resilience.

Adding extra insight to boost learnings from propositions testing

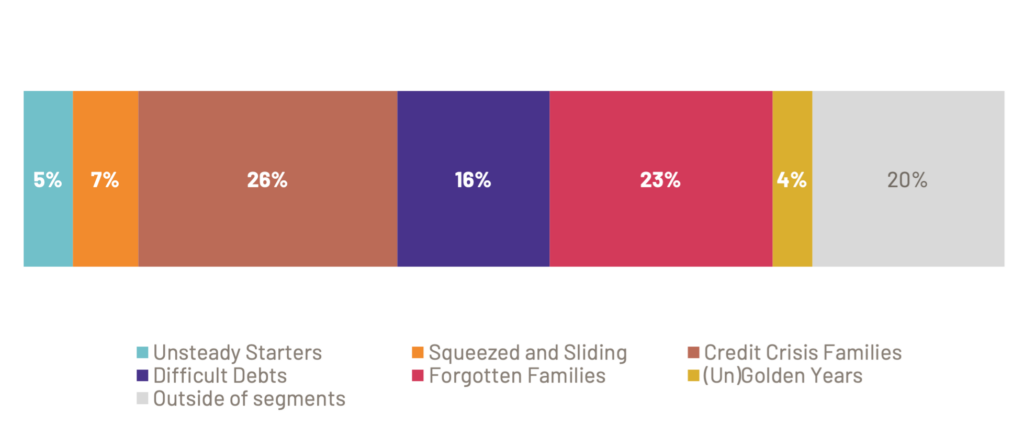

For the No Interest Loans Scheme, our hypothesis was that take-up would be highest for the two most financially vulnerable segments, Credit Crisis Families and Forgotten Families. After 4,475 loans, we mapped the customers to our segments.

While half are in these segments, the rest are split across the other segments (and some outside too).

Split of NILS customers by segment

How our segmentation model differs from others

Other studies show different, but similar numbers of people in financially or otherwise vulnerable circumstances:

- FCA Financial Lives Survey – almost 25 million people

- Plend Financial Inclusion Report – over 20 million people

- Totally Money and PwC – 23 million people

What’s important is that there is clearly a huge market that is under-served or excluded, and it’s going to take collaborative action to improve financial resilience.

Much of the variation will be based on methodology. As we’ve said above, our segmentation is less about ‘how many’ and more about ‘who’.

Often, a segmentation is based on demographic factors like age and income, particularly in financial services. This is easy to understand and works when you’re designing products around life stage and income levels.

Our segmentation is based on both demographics (largely age, income and family structure) and user needs (like if people are struggling with debt, their income doesn’t cover their monthly outgoings, and if they have used high cost credit)

We did this because we recognise financial vulnerability has complexities – for example you can be self employed on a reasonably high salary but still struggle to access products due to an irregular income, or on a lower income and be getting by well financially.

There are multiple ways to build a segmentation, each with their own opportunities and challenges:

Opportunities of a needs based segmentation

- Brings deep insight into needs and challenges that allows for more targeted product and service design

- Doesn’t oversimplify needs based on age and income (for example, there are people with the similar age and income level in credit crisis families and unsteady starters, but their circumstances and needs are very different)

- Can track changes of the needs of segments over time, and how interventions had made an impact to different groups

- If you have existing segmentation for your organisation, a needs based segmentation can add additional insight and depth to your segments

Challenges of a needs based segmentation

- Doesn’t provide as neatly defined groupings as demographic factors – needs are more nuanced and bring additional insight

- Harder to come up with an algorithm for matching the segments on quantitative data alone – much easier to match in qualitative scenarios when we can understand needs

- The segments give us a view of how many people overall, and we’re consciously cautious of scaling up data sets when it gets to sub-groups/smaller numbers. This is about understanding the needs of people, rather than ‘how many’ in each category.

What’s next

You can learn more about the 20.3m people in financially vulnerable circumstances here and sign up to access more segmentation insights and resources.

We’ve covered some of the different ways our segmentation can be used to drive change and boost financial inclusion. We’d love to hear from you if you have any other examples or ideas of what your organisation could do.

You can get in touch at hello@fair4allfinance.org.uk.